Accounting and analytical support for industrial enterprises. Accounting and analytical support for managing the sales processes of finished products in the organization

GENERAL DESCRIPTION OF WORK

Relevance of the research topic. Modern trends in the development of economic relations, increased competition to achieve competitive advantages and increased profitability of agricultural organizations require the use of fundamentally new approaches to management. This situation creates a need to have an information system capable of adequately and timely providing requests from managers at various levels of data management necessary to determine directions for further development and resolve current issues of production activities, including for effective cost management. The specificity of the production activities of agricultural producers is determined by a large set of internal and external factors and is manifested in a wide variety of areas of activity. For example, in crop production it is necessary to control the consumption of seeds, fertilizers, herbicides, etc. during sowing; In livestock farming, the rate of feed consumption should be taken into account. At the same time, we should not forget about the seasonality of production and the risks associated with weather conditions.

To assess the activities of agricultural organizations in general and identify specific factors that influence their final results, as well as develop options for management decisions for the management of organizations, a cost analysis is required. At the same time, the economic literature has not developed a methodology for analyzing costs that determines the characteristics of agricultural production.

All of the above allows us to say that the development of theoretical foundations, scientific and methodological provisions and practical recommendations for improving accounting and analytical support for cost management is relevant and timely at the present stage of economic development.

The degree of development of the problem. The works of domestic scientists such as P. S. Bezrukikh, I. N. Bogataya, M. A. Vakhrushina, O. N. Volkova, N. D. Vrublevsky, V. B. are devoted to the study of issues of theory and methodology of accounting support for cost management. Ivashkevich, T. P. Karpova, N. P. Kondrakov, M. I. Kuter, N. T. Labyntsev, S. A. Nikolaeva, V. F. Paliy, V. I. Podolsky, L. V. Popova, Y. V. Sokolov, V. I. Tkach, M. I. Trubochkina, V. T. Chaya, L. Z. Shneidman and others, as well as foreign scientists such as H. Anderson, A. Upchurch, J. Bethge, R. Braley, M. Van Breda, K. Drury, R. Kaplan, D. Caldwell, M. Matthews, D. Norton, B. Needles, M. Perera, J. Richard, K. Ward, J. Foster , E. Hendriksen, Schank, R. Anthony, et al.

A significant contribution to the development of the methodology for analytical support of cost management was made by domestic scientists: M. I. Bakanov, A. F. Ionova, M. V. Melnik, etc.

G. M. Lisovich, L. I. Khoruzhy, and others devoted their works to the problems of functioning and organization of the accounting and analytical support system in the field of agricultural production.

These research and developments are characterized by practical significance, being a significant contribution to the development of the theory and practice of accounting and analytical support for expenses. However, the insufficient use of accounting and analysis capabilities to satisfy user information requests about the costs of agricultural organizations for the purpose of effectively managing them determines the relevance of the chosen research topic, its practical significance and determines the purpose of the dissertation work, objectives, structure and content.

The purpose and objectives of the dissertation work. The purpose of the dissertation work is to develop theoretical, methodological and practical provisions for the formation of accounting and analytical support for cost management, aimed at increasing the efficiency of agricultural organizations.

In accordance with the purpose of the study, the following tasks were set:

1. Clarify theoretical ideas about the substantive characteristics of the concept of “costs”, “expenses” in order to develop the conceptual apparatus of the issue under study.

2. Explore the methodological support for accounting and analysis of expenses and ways to rationalize them.

3. To propose a methodology for analyzing costs within the framework of accounting and analytical support for cost management in agricultural organizations.

4. To develop a methodology for organizing management accounting of expenses in agricultural organizations, within the framework of which it is expected to improve the methodology for setting up management accounting of expenses and forming an expense budget.

5. Systematize the stages of accounting and analytical support for cost management in agricultural organizations.

6. Improve existing forms of accounting (financial) reporting regarding the organization’s expenses.

7. Develop forms of management reporting in relation to agricultural production.

Subject and object of research. Subject dissertation research is a set of theoretical, organizational and methodological issues of accounting and analytical support for managing expenses of agricultural organizations related to the formation of information about expenses in the system of financial, tax and management accounting.

Object Agricultural organizations of the Rostov region and Krasnodar region were selected for the study.

Theoretical and methodological basis of the study. The theoretical basis of the dissertation is the scientific works of leading domestic and foreign scientists and specialists in the field of accounting, economic analysis, materials from periodicals, legislative, regulatory and instructional acts devoted to the study of issues of accounting and cost analysis.

The research methodology is based on identifying the essence of expenses as an object of financial, tax, management accounting and analysis and justifying the need to improve accounting and analytical support for expense management.

The dissertation work was carried out in accordance with the Passport of the specialty of the Higher Attestation Commission (Economic Sciences) in the specialty 08.00.12 - accounting, statistics, section 1 “Accounting”, clause 1.7 “Accounting (financial, managerial, tax, etc.) accounting in organizations of various organizational and legal forms, all spheres and industries”, clause 1.8 “Features of the formation of accounting (financial, management, tax, etc.) reporting by industries, territories and other segments of economic activity”; section 2 “Economic analysis”, clause 2.11 “Theory and methodology of financial, managerial, tax, marketing analysis”, clause 2.14 “Analysis of assets and capital of business entities”.

The instrumental and methodological apparatus of the study is determined by the set of methods used in the study of accounting and analytical support for cost management in agricultural organizations. General scientific methods were used as tools: analysis, synthesis, induction, deduction, comparison, observation, consistency and complexity, formalization, analogy, historical, logical and systematic approaches, analytical, statistical, economic and mathematical methods, as well as methods of factor analysis, coefficient analysis. Special methods are used in the work: identification, measurement, forecasting.

The information and empirical base of the study was formed on the basis of legislative acts of the Russian Federation, decrees of the President of the Russian Federation, decrees and policy documents of the Government of the Russian Federation and other documents regulating the accounting of expenses, materials from periodicals, Internet resources, results of scientific works of domestic and foreign scientists presented in monographs, articles, as well as factual data on management and financial reporting of individual agricultural organizations in the Rostov region and Krasnodar region, author's developments.

Working hypothesis of dissertation research determined by the need to improve accounting and analytical support for cost management in agricultural organizations, which involves the development of theoretical and methodological provisions that will allow the formation of a modern approach to cost accounting and analysis, taking into account the needs of managers in accounting information and the results of its analysis for the purpose of making rational management decisions. The introduction of modern methods and techniques in the area under study by clarifying the terminological base, developing methods for analyzing expenses, and improving the forms of financial and management reporting will help improve management efficiency and informed decision-making on expense management in agricultural organizations.

The main provisions of the dissertation research submitted for defense.

1. Theoretical approaches to the concept and essence of expenses, costs, production costs, and production costs are characterized by a lack of unity and uniformity. The study of the definitions of these concepts made it possible to identify many points of view of domestic and foreign authors on this issue. This explains the need to develop a general approach to understanding the costs and expenses of an organization, based on an awareness of the role and significance of expenses in the system of accounting and analytical support for the management of an agricultural organization.

2. Features of production management are currently characterized by the fact that each agricultural organization needs to constantly compare income with expenses and draw up plans for further actions in the market. In this situation, cost analysis is an important tool for the effective functioning of organizations. Theoretical provisions and methods for analyzing expenses in agricultural organizations are characterized by an extremely insufficient level of research and require improvement. This determines the importance of developing an original methodology for cost analysis as a component of accounting and analytical support for cost management in order to provide analytical information when making management decisions.

The scientific novelty of the conducted research lies in the solution of theoretical, organizational and methodological issues of accounting and analytical support for cost management of agricultural organizations, which are of great importance for the development and improvement of the theory and practice of accounting and analysis. The main results containing scientific novelty were obtained in the following areas:

1. Theoretical ideas about the essence and content of the definition of “expenses” and “costs” have been developed and the author’s interpretation of these concepts has been substantiated, taking into account the specifics of agriculture, which differs from existing approaches to their definition. This will expand scientific understanding of the essence and content of expenses of agricultural organizations, taking into account their role in the accounting system as components of accounting and analytical support for making management decisions.

2. A methodology for analyzing expenses has been developed, adapted to the specifics of agricultural production and consisting of the following stages: 1) calculation of indicators of the dynamics and structure of expenses; 2) analysis of costs per 1 ruble of manufactured products; 3) calculation of the critical sales volume (break-even point); 4) factor analysis of expenses; 5) analysis of the impact of expenses on the profit and profitability of the organization. This technique will allow you to track expenses at any time, respond in a timely manner to various influences of the external and internal environment by making management decisions to regulate the expenses of an agricultural organization.

3. The stages of formation of accounting and analytical support for managing expenses of an agricultural organization are systematized, including: 1) determining the general principles of expense accounting; 2) development of a methodology for collecting and generating expenses from ordinary activities and other expenses; 3) analysis of the expenses of an agricultural organization; 4) setting up a management accounting system and creating management reporting based on it; 5) identification of promising areas for cost rationalization; 6) implementation of measures to rationalize the organization’s expenses. The implementation of this set of successive stages will help improve the accounting and analytical support for cost management in agricultural organizations by systematizing the listed processes.

4. The content of the accounting (financial) reporting form “Report on financial results” has been improved and supplemented by using the developed form for deciphering line 2120 “Cost of sales” (costs of crop production, livestock, processing, other costs) and line 2350 “Other expenses” in the context of the following components: depreciation of fixed assets, rent, difference in weight upon acceptance to the elevator, airport services, state duty, bank commission, travel expenses, preferential meals during agricultural work, exchange rate differences, financial assistance, charitable assistance, property tax, insurance accrual contributions, general business expenses, payment under a fee-based service agreement, payment for the negative impact of the environment, etc. The proposed additions will allow external and internal users to obtain detailed information when forming an opinion on the composition and structure of expenses of the organization for making certain management decisions, investing in the organization and etc.

5. Forms of management reporting have been developed in order to improve the documentation of expenses, including “Report on the implementation of cost estimates for growing crop products”, “Report on expenses and cost of production (work, services)”, “Calculation of cost of agricultural crops”. The use of these reporting forms, based on various characteristics and elements contained in them, corresponding to the objective information needs of managers when making management decisions, will allow for quick and more effective control of the costs of an agricultural organization.

Theoretical significance research is that the main provisions, conclusions and recommendations of the dissertation work deepen the theoretical and methodological aspects of accounting and analytical support for cost management and can be aimed at further theoretical research in this area, taking into account the current processes of accounting reform in the Russian Federation.

The practical significance of the dissertation research is to bring the research to the development and application of specific methods and practical recommendations aimed at improving the organization of accounting and analytical support for cost management in agricultural organizations, taking into account the specifics of this industry. The results of the study can be applied in the educational process of higher educational institutions.

Degree of reliability and testing of results. The results of the research were presented at intra-university, regional, international conferences and seminars at the Don State Agrarian University, Volgograd State Agrarian University, Yaroslavl State Agricultural Academy. The work was presented at the All-Russian competition for the best scientific work among students, graduate students and young scientists of higher educational institutions of the Ministry of Agriculture of the Russian Federation in the nomination “Economic Sciences”, where it took 1st place at the second stage of the competition in Volgograd.

The results of the dissertation work are used in the educational process of the Faculty of Economics of the Don State Agrarian University in the specialty 080109.65 “Accounting, Analysis and Audit” when conducting classes in the disciplines “Financial Accounting”, “Management Accounting”, “Accounting Financial Reporting”, “Cost Accounting” , calculation and budgeting in the industrial sectors of the agro-industrial complex”, “Comprehensive economic analysis of financial activities”.

Publications. The main provisions of the dissertation research are reflected in 17 scientific works with a total volume of 8.31 pp., of which 6.67 pp. are author's, including 3 articles in journals recommended by the Higher Attestation Commission, volume 2.76 pp., including copyright 2.01 pp.

Logical structure and scope of work. The dissertation consists of an introduction, three chapters, including 9 paragraphs, a conclusion, a bibliography and appendices. The work contains 29 figures, 31 tables, 12 formulas and 14 applications.

The dissertation work has the following structure.

Introduction

Chapter 1. Theoretical and methodological aspects of accounting and analysis of expenses in agricultural organizations

1.1. Comparative analysis of the definitions of the concepts of “costs”, “expenses”, “costs” and “cost”

1.2. Methodological aspects of cost accounting as an information base for making decisions on cost management

1.3. Information support for analysis of expenses of an agricultural organization

Chapter 2. Organization of accounting and analytical support for cost management

2.1. Analysis of modern methods for organizing financial accounting of expenses

2.2. Assessment of the organization of tax accounting of expenses of the organization

2.3. Features of the methodology for analyzing expenses in agricultural organizations

Chapter 3. Development of methods for organizing management accounting of expenses in agricultural organizations

3.1. Improving the methodology for setting up a management accounting system for expenses in agricultural organizations

3.2. Formation of expenditure budgets in agricultural organizations

3.3. Development of management reporting forms regarding expenses of agricultural organizations

Conclusion

Bibliography

Applications

MAIN CONTENT OF THE WORK

In administered the relevance of the dissertation work is substantiated, a description of the degree of knowledge of the issue is provided, the subject and object of the research are determined, the goal and objectives are formed, the provisions of the scientific novelty and practical significance of the dissertation work are given.

In the first chapter, “Theoretical and methodological aspects of accounting and analysis of expenses in agricultural organizations,” the essence of the accounting and analytical system of agricultural organizations is examined through the analysis of foreign and domestic literature.

All organizations, including agricultural ones, incur high costs, which forces management to look for ways to reduce this component of any activity process. Accounting and analytical software is a management tool for managing expenses. Accounting employees provide information about the organization's expenses, which is then analyzed and provided for further use. This complex requires a well-organized accounting system in general and expenses in the first place.

The study established that the cost management accounting system is an information system that should provide the management of agricultural organizations with the data necessary to make informed management decisions, including for solving the following tasks:

Increasing the efficiency of control over the organization's expenses;

Reducing ineffective expenses, i.e. expenses that arise when normal conditions of economic activity are violated;

Increasing production volumes of profitable types of products (works, services).

Determining the economic essence and content of expenses, costs, and prime costs is one of the ambiguous, controversial and not yet fully resolved issues in the theory and methodology of accounting. In the course of studying this issue, a review of views on the definitions of “costs”, “expenses”, “cost”, “expenses” made it possible to determine the main similarities and differences between them. In connection with this, the author has proposed refined definitions of these terms. The costs of an agricultural organization are understood as resources in monetary terms used in the production and sale of agricultural products, works and services for a certain period of time. Expenses are the disposal of assets of an agricultural organization and (or) an increase in accounts payable in the process of generating income (production and sale of agricultural products, provision of services or other activities), which leads to a decrease in its equity capital.

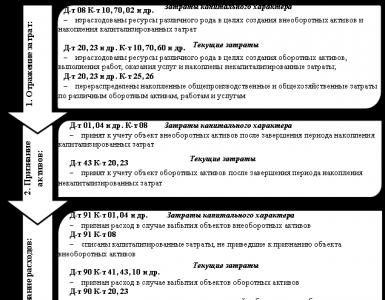

Picture 1 - Cost and Expense Accounting Scheme

As part of the dissertation work, the classification, principles of accounting and documentation of costs were studied. When making decisions on cost management based on cost information, it is necessary to clearly define large groups of sources of cost information that will be used by the heads of structural divisions of agricultural organizations. The author has systematized various reporting forms and accounting documents that can be used when making decisions on cost management in agricultural organizations, presented in Table 1.

Table 1 - List of accounting sources of information on costs

and the cost of agricultural products

Information sources |

|||

Registers synthetic accounting | Reporting forms |

||

Cost accounting sheet (form No. 301-APK), order journal | Production report (form No. 83-APK), sheet of analytical accounting of production costs (form) | Balance sheet (page 1210); Statement of financial results (pages 2120, 2210, 2220, 2330, 2350); Explanations to the balance sheet and income statement (subsection “Production costs”); f. No. 8 APK “Report on the costs of main production” |

|

Cost price | Journal-warrant No. 10-APK | Annual report “Information on production, costs, cost and sales of crop products” (f.), “Report on production, cost, sales of livestock products” (form No. 13-APK), statement of analytical accounting of production costs (f.) | Income statement; Explanations to the balance sheet and income statement; various types of calculations (planned, standard, actual); f. No. 9, 13 APK |

Journal warrant No. 10-APK, No. 11-APK | Statements of accounting for other income and expenses (form), register of documents on the sale of inventory, works and services (form No. 64-APK), sheet of analytical accounting of production costs (form) | Statement of financial results (pages 2120, 2210, 2220, 2330, 2350); Explanations to the balance sheet and income statement (subsection “Production costs”); f. No. 8 APK “Report on the costs of main production” |

The author has established that economic analysis in general and analysis of costs for the production and sale of agricultural products represent an objectively necessary element of production management. The main advantages of effective analysis of an organization's expenses include:

Increasing the competitiveness of manufactured products on the market by reducing their cost;

Availability of prompt and reliable information about the structure of product costs and the possibility of comparing it with the products of other organizations;

The ability to analytically substantiate the pricing policy of an agricultural organization and increase its flexibility;

Providing objective information for short-term and long-term financial planning and budgeting;

The ability to assess the contribution of each internal division of the organization to the creation of financial results;

Justification of rational management decisions.

As part of the study of cost analysis, the features of the methods of various authors were considered, which made it possible to conclude that many of them are similar in most respects. Thus, the study of theoretical and methodological aspects of accounting and analysis of expenses in agricultural organizations made it possible to determine the main directions of development of this problem.

In second chapter "Organization of accounting and analytical support for cost management" The issues of organizing modern methods and techniques of accounting and analytical support for cost management, which are becoming the most important conditions for increasing the efficiency of an organization in an environment of increased competition, are considered.

The author has studied the features of accounting support for expenses, their composition and classification, and identified the features of accounting support for expenses of an agricultural organization. The object of the study was the expenses of the South of Rus'” branch of the “Pridonsky Breeding Plant” of the Oktyabrsky district of the Rostov region.

We have established that in order to meet the needs of the management apparatus for information support, it is necessary to develop new and improve existing sources of information. The most informative in terms of income and expenses incurred is the Statement of Financial Results. Thus, the Statement of Financial Results in terms of expenses for ordinary activities and other expenses should be provided in an expanded form, in the form of the decoding we proposed (Table 2).

In the second chapter of the study, we studied tax accounting of expenses. The paper presents the characteristics of expenses from the point of view of tax accounting. Thus, in tax accounting, expenses are recognized as justified and documented expenses (and in cases provided for in Article 265 of the Tax Code of the Russian Federation, losses) incurred (incurred) by the taxpayer.

The main task, in our opinion, is to change the concept of tax accounting for the management of organizations, since currently there is a focus on the fiscal authorities in relation to profits received and, accordingly, expenses incurred, which makes reporting for external interested users insufficiently reliable, unlike Western practice, where accounting data serves as the main indicator of the organization’s performance for investors.

Table 2 - Example of decoding line 2120 “Cost of sales”

and 2350 “Other expenses” of the Statement of Financial Results"

|

lines | Indicators | Amount, rub. |

Cost of sales | ||

Crop production | ||

Livestock | ||

Recycling | ||

Other costs (goods, works and services) | ||

other expenses | ||

Depreciation of fixed assets | ||

Difference in weight upon delivery to the elevator | ||

Airport services | ||

State duty | ||

Commission of the bank | ||

Travel expenses | ||

Exchange differences | ||

Reduced food during agricultural work | ||

Material aid | ||

Charitable help | ||

Property tax | ||

Calculation of insurance premiums | ||

General running costs | ||

Payment under a fee-based service agreement | ||

Payment for negative impact on the environment | ||

Benefit payments | ||

Carrying out celebrations | ||

Sale of fixed assets | ||

Sale of goods and materials | ||

Repair of rented vehicles | ||

Write-off of fixed assets | ||

Write-off of inventory items | ||

Scholarship for students of agricultural universities | ||

Property insurance | ||

Cleaning the area | ||

Bank services | ||

Communication services |

Figure 2 – Stages of conducting a cost analysis

agricultural organizations

The preliminary stage of analyzing the expenses of an agricultural organization is the analysis of the provisions of the accounting policies governing the accounting of expenses.

The first stage “Calculation of indicators of the dynamics and structure of expenses” of the author’s methodology includes an analysis of the dynamics and structure of expenses of an agricultural organization. The structure of expenses should be analyzed by areas of activity (crop production, livestock production), cost elements (material costs, labor costs, etc.) and costing items (seeds and planting material, mineral and organic fertilizers, feed, maintenance and operation of fixed assets , property insurance costs, etc.).

The second stage of the methodology involves calculating indicators of product resource intensity. The purpose of this analysis is to establish specific costs per 1 ruble of revenue and track their dynamics, which characterize trends in changes in the efficiency of resource use. Costs per 1 ruble show the cost of one ruble of impersonal products and are determined by dividing the total cost of manufactured products by the cost of these products in current prices (excluding VAT). At a level of this indicator below one, agricultural production is considered profitable, and at a level above one – unprofitable.

At the third stage, the break-even point is calculated or the critical sales volume is analyzed, which allows one to assess the degree of commercial reliability of the organization, that is, its resistance to a decrease in demand and, accordingly, sales volume. It is based on the relationship between production volume (sales), cost and profit. It is based on the classification of costs in relation to production volume into variable and constant.

The fourth stage of the methodology is based on factor analysis of expenses. The analysis process reveals the influence of the following factors on the amount of expenses: sales volume of products, inflation rate, material intensity, salary intensity, depreciation intensity, resource intensity for other costs.

At the fifth stage, profitability indicators are analyzed. They characterize relative profitability, or profitability, measured as a percentage of the cost of funds or property. These indicators are among the most important, as they characterize the economic efficiency of agricultural production. They reflect the results of expenses not only of living, but also of past, embodied labor, the quality of agricultural products sold, the level of organization of production and its management.

The cost analysis methodology we propose will allow agricultural organizations to quickly make management decisions, as well as build a strategy for further development by rationalizing costs and finding new reserves for increasing competitiveness in the market.

The need for practical application of the analysis of expenses of agricultural organizations is caused by the importance of the results obtained and the conclusions drawn on their basis. This fact led to the implementation of analytical procedures at specific agricultural organizations: South of Rus', branch of the Pridonsky Breeding Plant of the Oktyabrsky district of the Rostov region and the Kushchevsky district of the Krasnodar Territory.

Discussed within third chapter dissertation work “Development of methods for organizing management accounting of expenses in agricultural organizations” Issues related to identifying the features of management accounting in agricultural organizations made it possible to identify and systematize the stages of accounting and analytical support for cost management in agricultural organizations.

As part of the study, we established that the ultimate goal of the study should be to determine the main directions for managing the costs of agricultural organizations to optimize them. In the course of analyzing existing methods, we came to the conclusion that accounting and analytical support for cost management in agricultural organizations involves the implementation of a whole range of activities (Fig. 3), which will ultimately rationalize costs.

Figure 4 – Management accounting in the information field

organizations

Management accounting has been one of the subjects of deep research for many years and is a promising direction for the development of accounting in the world. After studying various points of view of both domestic and foreign scientists, common views on the definition of management accounting were noted. Thus, management accounting is a system for recording, summarizing and presenting information about the economic activities of an organization necessary for management personnel to plan, control and manage these activities. The author analyzed the basic principles, goals, and objectives of management accounting.

The study proved that the key task of implementing management accounting is not to completely unify the enterprise’s accounting systems, but to ensure the closest integration between them. At the same time, in relation to accounting and financial reporting, it is important to adhere to the principle of horizontal integration with them of management accounting, which presupposes the comparability of data in accounting blocks.

Based on an analysis of the practice and theory of organizing management accounting, the author has identified five stages of establishing management accounting in agricultural organizations (Fig. 5).

|

Figure 5 – Stages of setting up management accounting

in agricultural organizations

At the first stage of establishing management accounting, it is necessary to develop regulations for the collection, registration, storage and presentation of all information necessary for making management decisions, provide a description of the management accounting and reporting system, and create an accounting policy.

At the second stage, a unified system of accounts and accounting entries should be adopted and approved. A unified system is used with a single-circle (integrated) accounting system.

The third stage involves building a budgeting system by performing the following procedures: developing a budgeting scheme that reflects the main business processes; appointment of those responsible for drawing up budgets; development of budget forms; development of a methodology for filling out budget forms; development of interaction between financial responsibility centers (structural divisions) when setting up budgeting.

The development of internal management reporting at the fourth stage of establishing management accounting includes the creation of the structure and format of management reports, the development of basic classifiers of the management accounting system, organizational and time regulations for management reporting, a document flow schedule, organization of document storage, etc.

At the final, fifth stage, various analysis procedures are carried out in agricultural organizations, identifying deviations and making decisions to rationalize costs.

Thus, we have systematized and presented the main provisions of management accounting for agricultural organizations. The results obtained will help improve the quality of the accounting system and rationalize costs through proper management.

Good management involves not only analyzing the organization's past or current performance, but also assessing what may happen to it in the future. Planning and budgeting are one of the most complex control functions in the management accounting system. The main task of planning is to determine the sets of activities that must be carried out to achieve the organization's goals and the corresponding budgetary funds for their implementation.

Fixed assets

Fixed assets

Total for Section I

Current assets

Accounts receivable

Cash and cash equivalents

Total for Section II

Accounts payable

Other obligations

Total for Section V

Organizations form and develop a package of internal management reporting in accordance with the individual information needs of management.

One of the stages of the developed structure of accounting and analytical support for managing expenses of agricultural organizations is the creation of internal management reporting. Based on the results of a survey among management and accounting personnel of agricultural organizations, we identified the need to improve and develop internal management reporting that meets their needs. Based on this fact, in the course of the study we have developed and propose to use a “Report on the implementation of cost estimates”, which meets all the requirements for management reporting. This form contains all the necessary details, and also includes planned, actual data and their deviations for the following indicators: seeds and planting material, mineral fertilizers, organic fertilizers, plant protection chemicals, electricity, petroleum products, spare parts, repair and construction materials for repairs , payment for services and work performed by third parties (repair of equipment, soil chemicalization), labor costs, social contributions, depreciation, and other expenses. A report on the implementation of cost estimates must be drawn up by the heads of production areas (foreman) monthly separately for each technological stage of production. The use of this report will provide the management staff of agricultural organizations with information on the progress of the production process and the dynamics of costs.

The author also developed and proposed a report form on costs and costs of products (works, services) for agricultural organizations. The report includes a list of the following indicators: amount of actual costs - total, thousand rubles; amount of planned costs – total, thousand rubles; deviations of the cost amount (plan/actual, +, -); actual cost of production, rub./kg; planned cost of production, rub./kg; Product cost deviation (plan/actual, +, -), rub./kg. Numerical values for these indicators are given in the context of the crop products grown (for example, winter wheat, winter barley, etc.). The use of the developed report will facilitate timely control of the amount of actual costs and the cost of specific types of agricultural products.

As a result of the study of the development of management reporting forms regarding the expenses of agricultural organizations, we can conclude that this process is absolutely necessary, which is included in the general scheme of accounting and analytical support for expense management.

IN conclusion The main results of the study are formulated and a general conclusion is made that the methods developed and proposed by the author for the development of accounting and analytical support for expenses in agricultural organizations are universal in nature and can be used by agricultural organizations. This is their main advantage over other existing methods and techniques.

Articles in peer-reviewed scientific publications,

1. Kirichenko, characteristics of the concept of expenses in the international and domestic accounting system [Text] // Fundamental Research. – 2011. – No. 12. – 0.7 pp.

2. Kirichenko, accounting and analytical support of expenses in agricultural organizations [Text] / , // Audit and financial analysis. – 2012. – No. 3. – 1.5 pp., including 0.75 auto. p.l.

3. Kirichenko, issues of the current state of tax accounting of expenses of agricultural organizations [Text] // Audit and financial analysis. – 2013. – No. 2. – 0.56 pp.

Scientific articles and abstracts of reports

4. Kirichenko, -analytical support for cost management in agricultural organizations [Text] // Accounting and analytical tools for forecasting the economic security of innovative development of territories: materials of the III International. scientific Conf., November 26–27, 2010 / Astrakhan. state tech. univ. – Astrakhan: ASTU Publishing House, 2013. – 0.56 pp.

5. Kirichenko, definitions of the concept of “costs” and their classification as components of the expenses of agricultural organizations [Text] // Innovations in science, education and business - the basis for the effective development of the agro-industrial complex: materials of the international. scientific-practical conf. February 1–4, 2011 – village. Persianovsky: DonGAU Publishing House, 2011. – 0.38 pp.

6. Kirichenko, accounting of expenses of agricultural organizations [Text] // Current problems of modern economics and ways to solve them: materials of the international. scientific-practical conf. students and graduate students, March 2–4, 2011 – village. Persianovsky: DonGAU Publishing House, 2011. – 0.5 pp.

7. Kirichenko, accounting for expenses of agricultural organizations [Text] // Strategy for sustainable development of the economy in a dynamic competitive environment: materials of the international. scientific-practical conf. - village Persianovsky: DonGAU Publishing House, 2011. – 0.38 pp.

8. Kirichenko, aspects of analytical support for cost management in agricultural organizations [Text] // Problems and trends in the innovative development of the agro-industrial complex and agricultural education in Russia: materials of the international. scientific-practical Conf., February 7–10, 2012 – village. Persianovsky: DonGAU Publishing House, 2012. – T. IV. – 0.25 p.l.

9. Kirichenko, issues of accounting and analytical support for cost management in agricultural organizations [Text] / , // Innovative ways of development of the agro-industrial complex: tasks and prospects: international. Sat. scientific tr. / Federal State Budgetary Educational Institution of Higher Professional Education "ACHAA". – Zernograd, 2012. – 0.5 p.l., including 0.25 auto. p.l.

10. Kirichenko, accounting of expenses in agricultural organizations on the example of the South of Rus'” branch of the “Pridonsky Breeding Plant” of the Oktyabrsky district of the Rostov region [Text] / , // Long-term socio-economic development of Russia: Purpose, priorities, mechanisms, tools: materials of the international. scientific-practical conf. - Persianovsky village, 2012. - 0.44 p.l., including 0.22 aut. p.l.

11. Kirichenko, fundamentals and practical application of analysis of expenses of agricultural organizations [Text] // Innovation and investment activity in the agro-industrial complex of the regions: materials of the international. scientific-practical conf., dedicated 75th anniversary of Rost. region, Rostov-on-Don-Zernograd, September-Oct. 2012 / Growth. state economy University (RINH); GNU VNIIEiN Russian Agricultural Academy. – Rostov n/d, 2012. – 0.47 p.l.

12. Kirichenko, cost analysis as a component of accounting and analytical support for management in agricultural organizations [Text] / // Improving accounting, analysis and auditing in accordance with International Financial Reporting Standards: materials of international. scientific-practical conf. within the framework of the International Congress “Eurasianism as the basis for sustainable development of the world community in the context of globalization” (Ekaterinburg, October 18, 2012): in 3 hours / [rep. per issue]. – Ekaterinburg: Ural Publishing House. state economy University, 2012. – Part 3. Directions: 8. Improving economic analysis in the context of using modern models of corporate governance; 9. Automation of accounting processes and reporting according to IFRS; 10. Audit of consolidated financial statements according to IFRS; 11. Differences in accounting and reporting principles in different countries; problems of their harmonization. – 0.25 p.l.

13. Kirichenko, issues of accounting for other expenses in agricultural organizations [Text] / // Current problems of socio-economic, political and legal development of modern Russia: materials of the III All-Russian. scientific-practical conf. Teaching staff, students, graduate students and young scientists, November 27, 2012 / Rost. state economy University (RINH). – Rostov n/d, 2012. – 0.36 p.l.

14. Kirichenko, management accounting of expenses [Text] / // The current stage of development of accounting, control and audit: trends, problems, prospects: materials of the 3rd International. scientific-practical Conf., December 7–8, 2012 - Sochi, 2012. - 0.34 pp.

15. Kirichenko, accounting information for management accounting purposes [Text] // Agricultural science, creativity, growth: materials of the international. scientific-practical conf. T. 1. Prospects for the development of accounting and analytical work at enterprises in various sectors of the economy (Section of the Faculty of Accounting and Finance). Part 1. – Stavropol: AGRUS Stavropol State. agrarian University, 2013. – 0.22 p.l.

16. Kirichenko, aspects of management accounting [Text] / , // Modern economic policy: priorities, strategies, mechanism: materials of the international. scientific-practical Conf., April 24–26, 2013 - Persianovsky village: DonGAU Publishing House, 2013. - 0.2 pp., including 0.1 author. p.l.

17. Kirichenko, budget expenditures in agricultural organizations [Text] / , // Models of agricultural development in the new economy: tools, forms, risks: materials of the international. scientific-practical conf., Rostov-on-Don, September 2013 - Rostov n/a: State Scientific Institution VNIIEiN of the Russian Agricultural Academy, 2013. - 0.7 pp., including 0.35 author. P.

Contents of the dissertation Candidate of Economic Sciences Kravchenko, Alena Andreevna

Theoretical foundations of accounting and analytical support of the organization's fixed assets.1. accounting and analytical support for basic management tools of the organization. nomic and accounting content of the basic categories of provision of fixed assets."

Recommended list of dissertations

Strategic accounting of depreciation of fixed assets in agricultural organizations 2007, Candidate of Economic Sciences Fetskovich, Igor Vladimirovich

The concept of depreciation and its accounting and analytical solution 2009, Candidate of Economic Sciences Vinogradova, Evgenia Aleksandrovna

Organization of accounting of fixed assets in agricultural organizations 2006, Candidate of Economic Sciences Amelina, Yulia Olegovna

Depreciation of fixed assets as an element of accounting policy in agricultural formations: the example of enterprises in the Pskov region 2007, Candidate of Economic Sciences Ivanova, Raisa Ivanovna

Improving the classification of fixed assets and depreciation policy in the accounting and tax accounting system: using the example of agro-industrial complex organizations in the Oryol region 2007, Candidate of Economic Sciences Okuneva, Irina Igorevna

Introduction of the dissertation (part of the abstract) on the topic “Accounting and analytical support for the management of fixed assets of agricultural organizations”

Relevance of the research topic. The state of fixed assets and the possibility of their renewal determine the level of competitiveness of domestic production, as well as the prerequisites for the development of the economy as a whole.

In modern conditions, increasing the efficiency of the process of reproduction and use of fixed assets in agricultural organizations directly depends on the presence of an effective management system. This system represents a complex mechanism that combines the processes of accounting and economic analysis in order to create accounting and analytical support that allows the generation of objective information in accordance with interests of users* and directions of industry development.The development of economic relations based on market principles, the growth of investments in agriculture, innovative ways to update fixed assets, require improvement of accounting and analysis, adaptation of their methods* to the requirements of interested users.

This determined the need to develop theoretical and methodological provisions for the formation of accounting and analytical information* about fixed assets, sources of reproduction, and the results of the implementation of the reproduction process of an agricultural organization in order to develop and make effective management decisions. In this regard, research focused on the development of theoretical and methodological provisions for the formation of accounting and analytical support (AAS) for the management of fixed assets of an agricultural organization is relevant.

The degree of development of the problem. A significant contribution to the study of theoretical and methodological foundations in the field of accounting and the formation of information in financial statements about the organization’s fixed assets, their analysis from the point of view of the implementation of the reproduction process was made by such domestic authors as Alborov P.A., Bakanov M.I., Bank S.V. , Blank I.A., V.KD Bu da wei, P:G. Bunich, D.A. Baranov, Belov N.G., Bogataya I.N., Bezrukikh P.S., Bychkova S.M., Vaskin F.I., Gilyarovskaya L.T., Getman B:F., Govdya V.V. , Endovitsky D.A., Kovalev

V.V., Kokorev N.A., Kostyukova E.I., Krylov E.I., Kuter M.A., Lyubushin N.P., Melnik M.V., Mizikovsky E.A., Novodvorsky V.D., Paliy V.F., A.F. Patskalev, Pizengolts M.Z., Popova L.V., V.V. Regush, Rudanovsky A.P., Sokolov Ya.V., Tkach V.I., Khoruzhy L.I., Chirkova M.B., Sheremet A.D., Shcherbakova N.F., Shirobokov V.G. and etc.

To varying degrees, the problems of the formation and use of fixed assets, their accounting and analysis have been studied in the works of a number of foreign scientists: Anderson X., Berndt E.R., Bethge J., Birman G., Van Breda M.F., Bru

C.L., Gerstner P., Drury K., Keynes J.M., Caldwell D., McConnell K.P., Middleton D., Miller D., Matthews M.R., Needles B., Perera M.H.B. ., Richard J., Hendriksen E.S., Hoyer W., Fischer S., Schmalenbach E., Schumpeter I.A., Schmidt S. et al.

However, despite the presence of undoubted achievements in the area under study, the continuous process of economic development and its current state requires further research aimed at reflecting industry specifics in the formation of accounting and analytical support for the management of fixed assets of the organization, adaptation of methodological approaches to making management decisions to the requirements of internal and external users of accounting information, strengthening accounting functions during the construction and implementation of depreciation policy for the formation of fixed assets of an agricultural organization for the purposes of financial, tax and management accounting.

Insufficient knowledge of the noted issues and the need to develop theoretical and methodological provisions for the formation of accounting and analytical support for the management of fixed assets of agricultural organizations determined the purpose and objectives of the study.

Compliance of the dissertation topic with the requirements of the passport of the Higher Attestation Commission (in economic sciences). The study was carried out within the framework. specialty 08.00.12 “Accounting, statistics” and corresponds to clause 1.4. “Methodological foundations and targets; accounting and economic analysis”, clause 1.8. “Accounting, and organization of various organizational and legal forms, all spheres and industries” Passports of specialties of the Higher Attestation Commission of the Ministry of Education and Science of the Russian Federation (economic sciences).

The purpose and objectives of dissertation research. The purpose of the dissertation work; consists in the development of theoretical and methodological provisions for accounting and analytical support for management; the main means of an agricultural organization. The formulated purpose of the study determined the need to solve the following problems: development of the theoretical foundations of accounting and analytical support; management of the organization's fixed assets; disclosure of the accounting content of the categories “fixed capital”, “fixed assets” and “fixed assets”, determining the relationship between them and their elements; justification of classification characteristics of fixed assets of an agricultural organization c. in the context of research into accounting and analytical support for management processes of an economic entity; development of methodological provisions for analyzing the policy of forming fixed assets of an agricultural organization; building a model for the formation of analytical procedures depending on the composition of the information base for the analysis of fixed assets of an agricultural organization;

Rationale. accounting and analytical model for depreciation policy in the formation of fixed assets of an agricultural organization.

The subject of the study is a set of theoretical and methodological issues of accounting and analytical support for the management of fixed assets of an organization.

The object of the study is the accounting and analytical processes of managing fixed assets in agricultural organizations in the conditions of reform and adaptation of Russian accounting to international standards.

The theoretical and methodological basis of the dissertation work was the scientific works of domestic and foreign authors devoted to the issues of accounting and analysis of fixed assets of organizations, legislative and regulatory acts on accounting and reporting, accounting standards, materials of scientific conferences, articles in scientific publications, monographic studies. In the process of work, general scientific methods of cognition were used as research tools, such as analysis and synthesis, modeling, concretization and abstraction - methods of statistical classification, groupings; historical and logical, systematic and comprehensive approaches were used to obtain evidence and argumentation of new provisions of the dissertation work.

The information basis was data from the Federal State Statistics Service, statistical and accounting reports of agricultural organizations in the Stavropol Territory, as well as the results of sample surveys of enterprises carried out by the author during the work.

The scientific novelty of the dissertation research “lies in the improvement of theoretical principles and the development of methodological tools for accounting and analytical support for the management of the main assets of an agricultural organization. The increase in scientific knowledge obtained in the dissertation is represented by the following elements:

Theoretical ideas about “accounting and analytical support for the management of fixed assets” have been expanded in part 1—clarification of the concept of “accounting and analytical support” and determining its place in the organization’s management system, as well as the justification of the structural model of the management of fixed assets, including five interconnected blocks;

The necessity of distinguishing the constituent elements of fixed capital in the presence of theoretical and functional contradictions between the categories “fixed assets”, “fixed assets”, “fixed capital” is proved and the relationship between them is shown, which made it possible to methodically substantiate the multifunctionality of fixed assets for the development of an assessment mechanism for the influence of their relationship on a number of key characteristics of the functioning of an economic entity;

Classification characteristics of fixed assets are identified (by degree of exposure to environmental risks, by stages of the organization's life cycle, by the level of generation of economic benefits, by types of policies regarding the capital supply process, by methods of education, etc.) and the corresponding groups of assets, which are given a linguistic characteristics from the point of view of the impact on the tools of accounting and analytical support for the management of fixed assets;

A methodological approach has been proposed for identifying policies for the formation of fixed capital, within which a procedure for analytical actions has been developed, including the identification of an identification feature, the structuring of user information requests and a differentiated system of indicators within the framework of technical, economic, financial, investment, innovation and environmental policies;

A model for distinguishing analytical actions depending on the composition and volume of the information base for carrying out calculation procedures is substantiated, allowing for a detailed comprehensive diagnosis of the state of fixed assets and an individualized assessment of the policy regarding the formation of: fixed assets of an agricultural organization;

An accounting and analytical model of differentiated selection and implementation of depreciation policy for the formation of fixed assets of an agricultural organization for the purposes of financial, tax and management accounting has been developed and tested.

The practical significance of the results of the dissertation research lies in the possibility of widespread use of the developed methods and models of accounting and analytical support for the management of fixed assets of an agricultural organization. Theoretical results have been brought to practical conclusions and organizational and methodological recommendations used in the economic practice of agricultural organizations of the Stavropol Territory, which is confirmed by certificates: on: implementation. The following have independent practical significance: *

Classification characteristics of fixed assets that meet the needs of creating accounting and analytical support. management processes of an agricultural organization;

Methodological provisions defining the procedure for identifying the policy for the formation of fixed assets of an agricultural organization;<

A model for delimiting analytical actions, depending on the composition and volume of the information base for analyzing the fixed assets of an agricultural organization;

Accounting and analytical model of differentiated selection and implementation of depreciation policy - formation - of fixed assets of agricultural organizations; "

Approbation of research results. The main results of the study were reported and received approval at international, all-Russian, regional scientific conferences in Knyagino, Moscow, Stavropol, Pyatigorsk, Cherkessk in 2005-2011.

The developed methodological provisions and practical recommendations have been implemented and used in agricultural organizations of the Stavropol Territory: the Orlovsky collective farm (implementation act dated 06/15/2011) and in the Department of Agriculture and Environmental Protection of the Administration of the Kirov Municipal District of the Stavropol Territory (implementation act dated 07/20/201 Gg.).

Scientific research results are used in the educational process of the North Caucasus State Technical University; (certificate of implementation dated 07/07/2011).

Publications. Based on the materials of the dissertation research, 13 printed works were published, in total; volume 3.59 p; l. (author's 3.59 pp:)^ including 3 articles in publications recommended by the Higher Attestation Commission of the Russian Federation. The volume and structure of the dissertation are determined by the purpose and tasks set and solved during the research. The work consists of an introduction, three chapters, a conclusion, a list of references; sources (224 titles), includes 34 tables, 27 figures, 5 appendices.

Similar dissertations in the specialty "Accounting, Statistics", 08.00.12 code VAK

Improving accounting of depreciation processes 2009, Candidate of Economic Sciences Mamedov, Rashad Ilham Ogly

Improving depreciation policy in agricultural organizations: accounting and tax aspects 2007, Candidate of Economic Sciences Kostyukov, Konstantin Ivanovich

Methodology for the formation of accounting and analytical support for the management of fixed capital in agricultural organizations 2011, Doctor of Economics Pronyaeva, Lyudmila Ivanovna

Accounting and analysis of the reproduction of fixed assets in the context of adaptation to IFRS requirements in agricultural organizations 2011, Candidate of Economic Sciences Agoshkova, Natalia Nikolaevna

Analysis of the reproduction of fixed assets and the formation of depreciation policy in agriculture: based on materials from organizations of the Orenburg region 2009, Candidate of Economic Sciences Ivanova, Yulia Olegovna

Conclusion of the dissertation on the topic “Accounting, Statistics”, Kravchenko, Alena Andreevna

Conclusion

Based on the research carried out in the work on the problem of accounting and analytical support for the management of fixed assets of agricultural organizations and the developed theoretical and practical provisions, the following conclusions and proposals were made:

1. The system of accounting, analytical support and organizational management plays a key role in the functioning of the management system, ensuring the interaction of different structural units, responding to external and internal changes. Accounting and analytical support is an integrated system that includes accounting (financial, tax, management), planning, control, analysis of the work of an agricultural organization in the context of business processes and responsibility centers, in order to make management decisions to improve production, reduce costs and improving the financial results of the organization.

2. Accounting and analytical support should be considered as a tool for effective management of the organization. This process must be examined in detail by type of property, since the conceptual apparatus, accounting, analytical and other sections will differ depending on the type of property or source. Thus, we have developed a model of accounting and analytical support for the management of fixed assets. The model contains five interconnected blocks reflecting accounting and analytical information on the formation and management of fixed assets. These include: 1. Conceptual apparatus.2. Investment and innovation tools. 3. Accounting tools. 4. Analytical tools." 5. Management tools.

3. In modern conditions, fixed assets act as a basic element of the potential of a production organization, distinguished by their multifunctionality. Fixed assets are substantiated as an element of an asset, means of labor, a property complex, an object of taxation, an object of collateral, a source of environmental pollution, etc., which in turn provides the basis for the development* of an assessment mechanism for the influence of fixed assets on a number of key characteristics of the functioning of a production organization (in The work identified the mechanism of influence of fixed assets on the intermediate and final results of the activities of an agricultural organization).

4. Depreciable property is a special type of business resources of an organization that are used for a long time in the production process and require a gradual transfer of value to a newly created product in order to create additional financial resources necessary for the reproduction process and revitalization of the investment activities of agricultural organizations.

5. To meet the needs of accounting and analytical activities of agricultural organizations, fixed assets should be classified according to 20 criteria (by the degree of exposure to environmental risks, by the stages of the organization’s life cycle, by the level of generation of economic benefits, by distribution between business segments, etc.).

6. The renewal coefficient was calculated, which expresses the share of fixed assets newly put into operation in the reporting year in the total cost of all fixed assets at the end of the year. Thus, from 2004 to 2008, there was a constant increase in this indicator. Only in 2009 does the renewal coefficient decrease, however, relative to 2004, its value is higher by 1.8. In 2009, it decreased by 1.1 and amounted to 1.2. In general, in Russia, the renewal rate of fixed assets in agriculture has been growing from 2004 to 2009, with only a slight decrease observed in 2009. In turn, the retirement rate for the period under study did not experience significant fluctuations, and from 2006 to 2009 its value remained unchanged.

7. The calculated depreciation rate expresses the degree of depreciation of fixed assets. From 2004 to 2009, there was a constant decrease in this coefficient, and in 2004 it amounted to 42.37%, in 2009 - 37.2%). The serviceability coefficient, which expresses the ratio of the residual value of fixed assets to their full (replacement) cost, changes in inverse proportion. Based on the calculations in the work, we can draw the following conclusion: the physical condition of the fixed assets of agriculture in Russia is characterized by an increasing degree of wear and tear, which confirms the need to renew the fixed assets of agriculture, at least for simple reproduction. The suitability indicator, in turn, increases. This fact confirms that fixed assets should not be repaired, but replaced with new ones.

8. Use the system of economic analysis of fixed assets and the procedure for identifying policies regarding the formation of fixed assets of an agricultural organization and a structured set of analytical actions of economic analysis.

9. To generate information about accrued amounts of depreciation accepted when calculating income tax, in our opinion, it would be advisable to open an additional subaccount 02.2 “Depreciation for tax purposes” to account 02 “Depreciation of fixed assets”.

10. In order to improve the efficiency of tax accounting in an organization, a second group of analytical accounts should be introduced into account 02 “Depreciation of fixed assets” and account 01 “Fixed assets”, which will allow generating information about the initial cost of fixed assets and the amount of accrued depreciation in the accounting and tax accounting:

02.1.1 - “Accrued depreciation in accounting”;

02.1.2 - “Accrued depreciation in tax accounting”;

01.9.1 - “Initial cost of fixed assets in accounting”;

01.9.2 - “Initial cost of depreciable property.” One of the most serious problems is the misuse of depreciation charges. To date, the depreciation fund has been liquidated as a financial asset of business entities. But if there is no depreciation fund as an accounting object, then the mechanisms to ensure its intended use cannot operate. In order to solve this problem, the work proposes to summarize information about the investment reserve for the reproduction of the organization's fixed assets on separate off-balance sheet accounts, which will ensure control over the intended use of the investment reserve funds and increase the reproduction function of depreciation.

11. Introduce an original calculation and analytical approach to the management of fixed assets through the management of depreciation charges for fixed assets for the purposes of financial, tax, and management accounting, which includes: factors that determine the prerequisites for the formation of depreciation policy (cost of fixed assets, methods of assessing fixed assets, useful life depreciable property, depreciation rates, composition and structure of fixed assets, etc.); choosing the appropriate method for calculating depreciation of fixed assets for accounting and tax purposes;

Accounting support for accrued depreciation;

Analysis of the chosen method of calculating depreciation;

Assessing its effectiveness.

12. The calculations made in the work confirm that using the linear method of calculating depreciation in relation to the active part of the organization’s fixed assets, namely vehicles, is inappropriate. This is explained by the uniform write-off of the cost of fixed assets throughout their entire standard service life, which negatively affects the formation and use of depreciation charges, which by the end of operation lose their purchasing power and do not ensure the full reproduction of fixed assets. In this regard, the work proposes the use of accelerated depreciation methods, which make it possible to write off most of the cost of fixed assets in the first years of their operation and, thereby, protect the organization from losses due to inflation and obsolescence of fixed assets. In order to increase the efficiency of management decisions, as well as increase the investment activity of the organization, methodological approaches are proposed and a mechanism for managing the depreciation of fixed assets is developed by assessing the influence of the depreciation method on the formation of cash flow.

List of references for dissertation research Candidate of Economic Sciences Kravchenko, Alena Andreevna, 2011

1. Russian Federation. Constitution 1993. Constitution of the Russian Federation: official. text. M:: Marketing, 200G. - 39 s.

2. Russian Federation. Laws. Civil Code of the Russian Federation. Part Ill: Federal Law of November 26, 2001 No. G46-F3; // Collection. legislation of the Russian Federation. 2002. - No. 34., - Art. 1759.

3. Russian Federation. Laws. Tax Code of the Russian Federation. Parts I and IT M.: IGTFRA-M, 2006. - 480 p.

4. Russian Federation. Laws. About accounting: Approved. by order of the Ministry of Finance of the Russian Federation dated November 21, 1996. No. 129-FZ // Fish gas. - 1996. No. 50. - P. 1-4:

5. Russian Federation. Government of the Russian Federation; On approval of the accounting reform program in accordance with international financial reporting standards: Resolution No. 283 of March 6, 1998.

6. Russian Federation. , Ministry of Finance. Concept for the development of accounting, accounting and reporting in the Russian Federation for the medium term: Approved. by order; Ministry of Finance of Russia dated July 1, 2004 No. 180.

7. Russian Federation. Ministry of Finance. Standard recommendations for organizing accounting for small businesses: Approved. by order of the Russian Ministry of Finance dated December 21. 1998 No. 64n.

8. Russian Federation. Ministry of Finance. Accounting Regulations “Accounting for Fixed Assets” (PBU 6/01): approved. By order

9. Ministry of Finance of Russia dated March 30, 2001 No. 26n // Accounting Regulations (LBU 1-19). 6th ed. - M;: INFRA-M, 2002. - 144 p.

10. Russian Federation. Ministry of Finance. . Accounting Regulations “Expenses of the Organization” (PBU 10/99): approved. By order of the Ministry of Finance of Russia dated May 6, 1999. No.ЗЗн//Accounting Regulations (PBU 1 19). - 6th ed. - M.: INFRA-M; 2002.-144 p.

11. Russian Federation. Ministry of Finance. Guidelines for accounting of fixed assets: Approved. by order of the Ministry of Finance of the Russian Federation dated October 13, 2003 No. 91n // Collection of laws of the Russian Federation.-2004.-No. 24.-Ct.1290.

12. Russian Federation. Government. Classification of fixed assets included in depreciation groups: Decree of the Government of the Russian Federation. Federation dated January 1, 2002, No. 1 // Ross., gas.-2003.- No. 8.-P.5. ■

13. Russian Federation. On uniform norms of depreciation deductions for the complete restoration of fixed assets of the national economy of the USSR: Postan. Council of Ministers of the USSR dated October 22, 1990. No. 1070 // Collection. Postan: Govt. THE USSR. 1990. - No. 29-30. - St. 140.

14. Russian Federation. On measures to improve the procedure and methods for determining depreciation charges: Regulations. Govt. RF dated December 31, 1997 No. 1612II Financial newspaper. 1998. - No. Z.-S. 9:

15. Russian Federation: On the revaluation of fixed assets in: 1997: Postan. Govt. RF dated December 7, 1996 No. 1442"7/Accounting" -1997.-No.2.-C 112. .

16. Russian Federation. On the procedure for providing state guarantees and placement of centralized resources: Resolution: Govt. RF No. 1470 dated 22:11.97.

17. Russian Federation. On clarifying the procedure for calculating depreciation charges and revaluation of fixed assets:. Regulation Govt. RF dated June 24, 1998 No. 627IIRus. gas. 1998. -July 2. - 0.3.

18. Russian Federation. On the main directions of tax reform in the Russian Federation and measures to strengthen discipline: Decree of the President of the Russian Federation of May 8, 1996. No. 6 // Collection. Legislation of the Russian Federation. 1996.- No. 20. - P. 4999 - 5000.

19. Russian Federation. On accelerated depreciation for personal computers: letter from the Ministry of Economy of Russia dated January 17, 2020. No. МВ -32/6 51 // Main accountant. No■ 1C.

20. Russian Federation. On clarifying the procedure for calculating ■ .depreciation charges and revaluation of fixed assets: Regulations. Govt. RF dated June 24, 1998 No. 627 // Accounting: Official materials: -1998. No. 8. - P. 20 - 23.

21. Russian Federation. About* inclusion of depreciation charges in the cost of products (works, services). Letter from the Ministry of Finance? RF \ dated December 17, 1996 No. 16-00-17-163.

22. Russian Federation. Decree of the Government of the Russian Federation dated 01.01.2002 N 1 (as amended on 08.08.2003) “On the classification of fixed assets included in: depreciation groups”

23. Russian Federation. “Letter” of the Ministry of Finance of the Russian Federation dated September 16-2002 N 16-001 14/359 “On accounting1 of fixed assets after the entry into force of Chapter 25 of the Tax Code of the Russian Federation”

24. Russian Federation. “Letter” of the Ministry of Finance of the Russian Federation dated October 21, 2004 N 07-0514/275 “On the calculation of depreciation on fixed assets, as well as on VAT deductions for the acquisition of land plots”

25. Russian Federation. “Letter” of the Ministry of Finance of the Russian Federation dated July 29, 2004: N 07-0514/199 “On the calculation of depreciation on intangible assets in the form of an exclusive right to a trademark”

26. Agro-industrial complex of Stavropol: Static: collection./ Ed. N.M. Nikolaev.:: Stavropol! Regional Committee of State Statistics, 2010. - 184 p.

27. Aniskin, Yu.P. Planning and controlling: Textbook / Yu.P. Aniskin, A.M. Pavlova;-M.: Omega-L, 2003. 280 p.

28. Astakhov, V.P. Accounting: financial accounting: Textbook / V.P.; Astakhov: M;: ICC “MarT”, 2001. - 832 p.

29. Astakhov, V.P. Accounting theory / V.P. Astakhov; -Publishing center "MarT", 2001. - 448 e.

30. Babaev, A.S. Accounting policy of the organization / A.C. Babaev, L.Z. Shneidman.- M;: Publishing house. “Accounting”, 2003.-112 p.

31. Bank, V.R. Financial analysis Text: textbook. Benefit / V.R. Bank, C.B. Bank, A.B. Taraskina.- M.: TK Welby. Prospekt Publishing House, 2005. 344 p.

32. Bakaev, A.S. Explanatory accounting dictionary. - M.: Publishing house "Accounting", 2006.-176p.

33. Binshtok, F.I. Pricing: Textbook. allowance / full name; Binstock. M.: INFRA-M, 2001. - 197 p.

34. Blank, I.A. Fundamentals of financial management. T.1 ./ I.A. Form. K.: Nika-Center, 1999. - 592 p. - (Series “Financial Manager Library”; Issue 3.

35. Blank, I.A. Fundamentals of financial management. T.2. / I.A. Form. K.: Nika-Center, 1999.- 512 p.

36. Blank, I.A. Profit management / I.A. Form. K.: “Nika - Center”, 1998.-544 p.

37. Bogataya, I.N. Accounting. Series "Higher Education". 3rd ed., revised. and additional / I.N. Rich, H.H. Khakhonova. Rostov n/d: “Phoenix”, 2004. - 800 p.

38. Bogataya, I.N.: Strategic accounting of enterprise property / I.N. Rich. Series “50(ways”). Rostov n/d.: “Phoenix”, 200k 320 pp.

39. Large economic dictionary / Ed. A.N. Azriliyana. - 4th ed. add. and processed -M.: Institute of New Economics, 1999. 1248 p.

40. Borodina, V.V. Accounting. Textbook / V.V. Borodin. -M.: Book World, 2002. 299 p.

41. Boronenkova, S.A. Economic analysis in enterprise management / S.A. Boronenkova. M.: Finance and Statistics, 2003. - 224 p.

42. Budavey V.Yu. Problems of depreciation in industry. M.: Finance, 1970.- 191 p.

43. Accounting (financial) accounting: Accounting for assets and settlement transactions. Textbook Benefit / V.A. Pipko, V.I. Berezhnoy, J1.H. Bulavin et al. M.: Finance and Statistics, 2002. - 416 p.

44. Accounting (financial) accounting: Accounting for production, capital, financial results and financial reporting: Textbook. allowance / Ed. Prof. V.A. Pipko: M.: Finance and Statistics, 2004. - 352 p.

45. Accounting: Textbook / I.I. Bochkareva, V.A. Bykov and others; Ed. I'M IN. Sokolova. M.: TK Welby, Prospekt Publishing House, 2004. - 768 p.

46. Accounting: Textbook for universities / Ed. Prof. Yu.A. Babaeva. M.: UNITY-DANA, 2001. - 476 p.

47. Bychkov, M.F. Accounting in agro-industrial complex enterprises: Textbook. Benefit / M.F. Bychkov. M.: Finance and Statistics, 2004. - 208 p.

48. Vakulenko, T.G. Analysis of accounting (financial) statements for making management decisions / T.G. Vakulenko, L.F.; Fomina. - St. Petersburg: “Gerda Publishing House”, 2001. 288 p.

49. Bakhrushina, M.A. Management analysis / M.A. Bakhrushin. M.: Omega-L; 2004. - 432 p.

50. Bakhrushina, M. A. Management accounting: Textbook for universities. 2nd ed., add. and lane / M. A. Bakhrushina. M.: IKF Omega-JI; High Shchk., 2002. 528 pp.

51. Veretennikova, I Ml Depreciation and depreciation policy Text: textbook. allowance / I.I. Veretennikova. -M:. Finance and Statistics, 2004. 192 p.

52. Vinogradova; E.A. Accounting concept of depreciation and its development Text./ E.A. Vinogradova // Siberian financial school: scientific and practical journal. 2009. - No. 2. - p. 17-19.

53. Bulletin of IPB: Issue 3. Directory of correspondence of accounting accounts / Ed. A.C. Bakaeva. M.: Institute of Professional Accountants of Russia: Information Agency "IPB - BINFA", 2002. - 608 p.

54. Getman, V.G. Financial accounting: textbook Text: textbook/ V.G. Getman, V. A. Terekhova. - M.: Publishing and trading corporation "Dashkov and Co", 2008. 496 p.

55. Getman, V.G. International Financial Reporting Standards Text: textbook / V.G. Getman. M.: Finance and statistics. 2009. - 656 p.

56. Gilyarovskaya, JI.T. Accounting for financial reserves of an enterprise Text./ JI.T. Gilyarovskaya, JI.A. Melnikova. St. Petersburg: Peter, 2003. - 192 p.

57. Cash: accounting, analysis, audit: Educational and practical manual /

58. B.A. Pipko, E.A. Batishcheva, E.I. Kostyukova, O.E. Sytnik; edited by V.A. Pipko. Stavropol: Publishing house StGAU "AGRUS", 2004. - 184 p.

59. Dzhaarbekov, S.M. Methods and schemes for tax optimization /

60. S.M. Jaarbekov. -M.: MCFR, 2004. 672 p.

61. Dymova, I.A. Accounting statements and principles of their preparation in accordance with international standards. Transformation technique / I.A. Dymova. - M.: Modern economics and law, 2001. - 160 p.

62. Dymova, I.A. International accounting standards / I.A. Dymova. M.: Glavbukh, 2000. - 156 p.